One of the most critical drivers of intercompany treasury efficiency is the design of your cash transfer and roll-up strategy. While intercompany activity can include inventory flows, expense allocations, and revenue alignment — this discussion focuses exclusively on cash movement.

Start with the Right Organizational Structure

It sounds basic — but the entity structure defines the efficiency of your treasury management. Poorly organized ownership structures create unnecessary lateral activity between subsidiaries, making cash control harder, reconciliation slower, and the month-end close more painful than it needs to be.

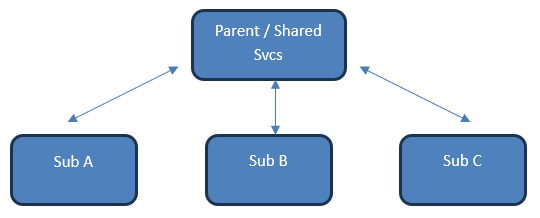

A best-practice design isolates cash into a single treasury account at the Parent or Shared Services entity — never at the subsidiary level.

Why This Works

Cash is rolled up and down only through the parent/shared services account. No lateral transfers between subsidiaries — ever.

Banks support this elegantly through Zero Balance Accounts (ZBAs), which allow automatic sweeps and rebalancing to maintain zero or minimum balances. When synced to the ERP, all transfers are instantly reflected, minimizing manual tasking.

The Math of Simplicity

Design Choice # of Intercompany Cash Accounts

Centralized (Best Practice) – Cash only moves 6 (3 Parent / Shared Services + 1 per parent ⇄ subsidiaries subsidiary)

Lateral Subsidiary Transfers Allowed 12+ (double the reconciliation work)

The Hidden Win: Faster Close, Less Risk

By eliminating cross-subsidiary activity and minimizing the number of intercompany relationships, companies can:

✅ Accelerate cash reconciliation

✅ Reduce intercompany accounting errors

✅ Simplify audit evidence

✅ Shorten the month-end close cycle

Cash structure is not an operational detail — it’s a control decision. The companies that centralize win on speed, accuracy, and liquidity visibility.